QQ登錄

QQ登錄 微博登錄

微博登錄 微信登錄

微信登錄

財(cái)務(wù)報(bào)告與分析中章節(jié)的設(shè)置是循序漸進(jìn)、逐層深入的,前面介紹的術(shù)語在后面還會(huì)有詳細(xì)的解釋與探討。

由于財(cái)務(wù)報(bào)告與分析本身自立體系,它是上市公司和報(bào)表使用人之間溝通交流的語言,所以學(xué)起來與外語學(xué)習(xí)有幾分相似。

財(cái)務(wù)報(bào)告與分析一共分為四大部分:

第一部分是掃盲階段,主要介紹財(cái)務(wù)術(shù)語、體系等基本知識(shí)。

在此基礎(chǔ)上,第二部分更深入地講解財(cái)務(wù)報(bào)表編制以及財(cái)務(wù)報(bào)表分析的方法。

進(jìn)一步地,第三部分針對(duì)存在利潤操縱空間的重點(diǎn)科目做詳細(xì)、深入的討論。

最后,第四部分是前面三部分內(nèi)容的綜合應(yīng)用。

四大部分在考試中占比最大的是第二部分和第三部分,大概占財(cái)報(bào)分析所有題目的80%以上。其次是第一部分,占比10%左右。

由于第四部分是財(cái)務(wù)分析的綜合應(yīng)用,不太適合一級(jí)的出題形式,所以出題比例相對(duì)比較少,大概占5%左右。

Questions 1:

At the end of the year,a company r*ued its manufacturing facilities,increasing their carrying amount by 12%.There had been no prior downward r*uation of these facilities.The r*uation will most likely cause the company’s:

A、return on assets to increase.

B、return on equity to decline.

C、net profit margin to increase.

【Answer to question 1】B

【analysis】

B is correct.The upward r*uation increases the carrying amount of the assets but bypasses net income.The r*uation is reported as other comprehensive income and will be accumulated in equity under the heading of r*uation surplus,increasing equity.This increase will cause the return on equity to decline.

A is incorrect.The upward r*uation causes an increase in the carrying amount of the assets but bypasses net income and is reported as other comprehensive income(under the heading of r*uation surplus),increasing equity.This will cause the return on assets to decline(same income,higher assets).

C is incorrect.The upward r*uation causes an increase in the carrying amount of the assets but bypasses net income and is reported as other comprehensive income(under the heading of r*uation surplus),increasing equity.This will cause Net Income/Sales to be unaffected.

Questions 2:

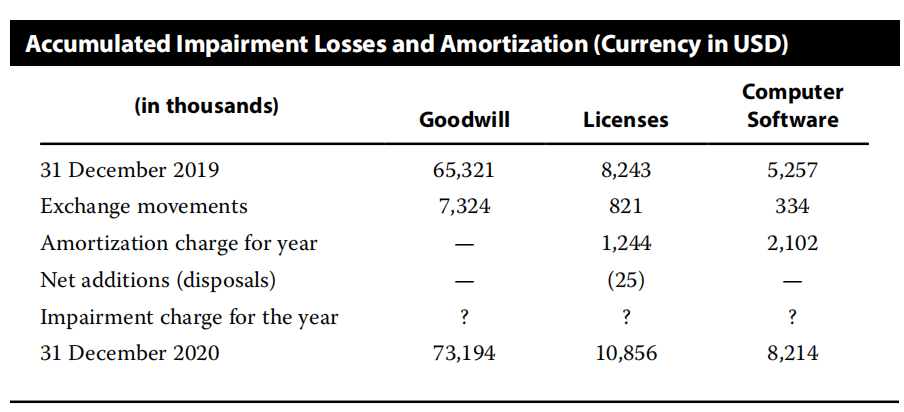

A technology company,reporting under US GAAP,has three classes of intangible assets.The table below shows information on each of the three classes.:

Based on the data provided,the intangible asset that has the largest absolute impairment charge for the period ended 31 December 31 2020,is:

A、computer software.

B、licenses.

C、goodwill.

【Answer to question 2】B

【analysis】

B is correct.Licenses will have the largest dollar impairment charge on the income statement due to the size of the implied impairment charge,which is calculated as:Accumulated impairment losses and amortization as of 31 December 2019–(Accumulated impairment losses and amortization as of 31 December 2019+Exchange movements+Amortization charge for year+Net Additions(Disposals)).In this case the largest impairment loss that will be reported is due to licenses.Impairment charge due to licenses=10,856–(8,243+821+1,244–25)=573.

A is incorrect because the amount of the impairment charge due to computer software is less than that of licenses.The computer software impairment charge for 20X2 in dollars=8,214–(5,257+334+2,102)=521.

C is incorrect because the amount of the impairment charge due to goodwill is less than that of licenses.The goodwill impairment charge for 20X2 in dollars=73,194–(65,321+7,324)=549.

相關(guān)閱讀

延伸閱讀

以上就是【CFA財(cái)務(wù)報(bào)表分析練習(xí)題之升值】的全部?jī)?nèi)容,如果你想學(xué)習(xí)更多CFA相關(guān)知識(shí),歡迎大家前往高頓教育官網(wǎng)CFA頻道!在這里,你可以學(xué)習(xí)更多精品課程,練習(xí)更多重點(diǎn)試題,了解更多最新考試動(dòng)態(tài)。