QQ登錄

QQ登錄 微博登錄

微博登錄 微信登錄

微信登錄

財務報告與分析中章節(jié)的設置是循序漸進、逐層深入的,前面介紹的術語在后面還會有詳細的解釋與探討。

由于財務報告與分析本身自立體系,它是上市公司和報表使用人之間溝通交流的語言,所以學起來與外語學習有幾分相似。

財務報告與分析一共分為四大部分:

第一部分是掃盲階段,主要介紹財務術語、體系等基本知識。

在此基礎上,第二部分更深入地講解財務報表編制以及財務報表分析的方法。

進一步地,第三部分針對存在利潤操縱空間的重點科目做詳細、深入的討論。

最后,第四部分是前面三部分內(nèi)容的綜合應用。

四大部分在考試中占比最大的是第二部分和第三部分,大概占財報分析所有題目的80%以上。其次是第一部分,占比10%左右。

由于第四部分是財務分析的綜合應用,不太適合一級的出題形式,所以出題比例相對比較少,大概占5%左右。

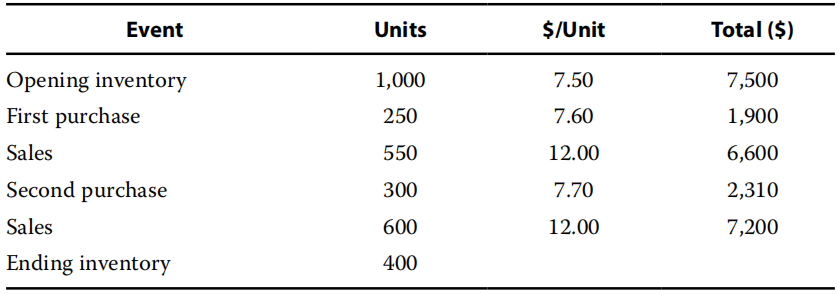

Questions 1:

Selected information from a company that uses the FIFO inventory method is

provided:

If the company used a perpetual system versus a periodic inventory system,the gross margin would most likely be:

A、higher.

B、lower.

C、the same.

【Answer to question 1】C

【analysis】

C is correct.When using the FIFO inventory method,the ending inventory,the cost of goods sold,and the gross margin are the same under either the perpetual or periodic methods.The use of a perpetual or periodic system makes a difference under the weighted average and LIFO methods.

A is incorrect.When using the FIFO inventory method,the cost of goods sold,and hence the gross margin,are the same under either the perpetual or periodic methods.

B is incorrect.When using the FIFO inventory method,the cost of goods sold,and hence the gross margin,are the same under either the perpetual or periodic methods.Under either method the oldest items are sold first.The first sale is 550 at$7.50.The next sale is 450 at$7.50+150 at$7.60.The perpetual and periodic methods make a difference under weighted average and LIFO.

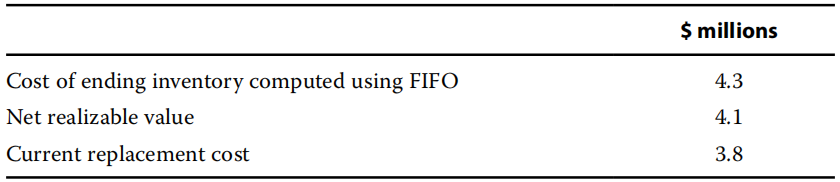

Questions 2:

The following information is available for a manufacturing company:

If the company is using International Financial Reporting Standards(IFRS)instead of US GAAP,its cost of goods sold(in millions)is most likely:

A、$0.3 higher.

B、$0.3 lower.

C、the same.

【Answer to question 2】B

【analysis】

B is correct.Under IFRS,the inventory would be written down to its net realizable value($4.1 million);under US GAAP,market value is defined as current replacement cost and thus would be written down to its current replacement cost($3.8 million).The smaller write-down under IFRS will reduce the amount charged to the cost of goods sold compared with US GAAP and result in a lower cost of goods sold of$0.3 million.

A is incorrect.The write-down is larger under US GAAP,so IFRS gross profit would be higher,not lower.

C is incorrect.IFRS and US GAAP define market differently.As current replacement cost(US GAAP definition is lower than NRV)the effect is not the same.

以上就是【CFA財務報表分析練習題"Financial Report":Inventories】的全部內(nèi)容,如果你想學習更多CFA相關知識,歡迎大家前往高頓教育官網(wǎng)CFA頻道!在這里,你可以學習更多精品課程,練習更多重點試題,了解更多最新考試動態(tài)。