QQ登錄

QQ登錄 微博登錄

微博登錄 微信登錄

微信登錄

CFA財(cái)務(wù)報(bào)表分析練習(xí)題"Financial Report":Understanding Income Statements

財(cái)務(wù)報(bào)告與分析中章節(jié)的設(shè)置是循序漸進(jìn)、逐層深入的,前面介紹的術(shù)語在后面還會(huì)有詳細(xì)的解釋與探討。

由于財(cái)務(wù)報(bào)告與分析本身自立體系,它是上市公司和報(bào)表使用人之間溝通交流的語言,所以學(xué)起來與外語學(xué)習(xí)有幾分相似。

財(cái)務(wù)報(bào)告與分析一共分為四大部分:

第一部分是掃盲階段,主要介紹財(cái)務(wù)術(shù)語、體系等基本知識(shí)。

在此基礎(chǔ)上,第二部分更深入地講解財(cái)務(wù)報(bào)表編制以及財(cái)務(wù)報(bào)表分析的方法。

進(jìn)一步地,第三部分針對(duì)存在利潤(rùn)操縱空間的重點(diǎn)科目做詳細(xì)、深入的討論。

最后,第四部分是前面三部分內(nèi)容的綜合應(yīng)用。

四大部分在考試中占比最大的是第二部分和第三部分,大概占財(cái)報(bào)分析所有題目的80%以上。其次是第一部分,占比10%左右。

由于第四部分是財(cái)務(wù)分析的綜合應(yīng)用,不太適合一級(jí)的出題形式,所以出題比例相對(duì)比較少,大概占5%左右。

Questions 1:

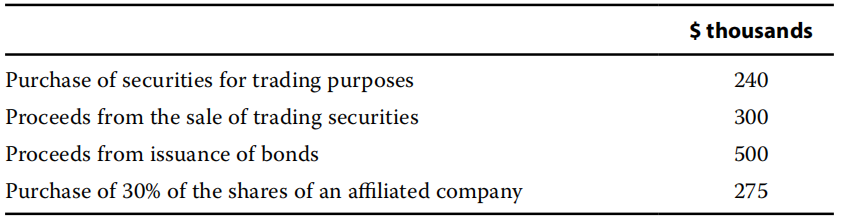

A company recorded the following events during 2014:

On the 2014 statement of cash flows,the company’s net cash flow from investing activities(in thousands)is closest to:

A、$285.

B、–$275.

C、–$215.

【Answer to question 1】B

【analysis】

B is correct.Only the cash flows for the purchase of the shares in an affiliated company is cash from investing activities,thus the net amount is–$275,000.Cash flows from trading securities is an operating activity,and cash flow from issuing bonds is a financing activity.

A is incorrect.It also includes the proceeds from the issuance of the bond,but that is a financing activity:–275,000–240,000+300,000+500,000=285,000.

C is incorrect.It includes the proceeds and purchase of the trading securities,but they are operating activities:–275,000–240,000+300,000=–215,000

Questions 2:

The converged revenue recognition standards(issued by the International Accounting Standards Board and the Financial Accounting Standards Board in May 2014)are best described as differing from pre-converged US GAAP in that they:

A、align the recognition of revenue with the customer’s fulfillment of payment obligations.

B、provide extensive additional guidance for specific industries and transactions.

C、provide a principles-based approach applicable to many types of revenuegenerating activities.

【Answer to question 2】C

【analysis】

C is correct.The converged standards aim to take a principles-based approach that avoids the provision of specific rules and requirements characteristic of current US GAAP revenue recognition standards.

A is incorrect.Neither current US GAAP nor the new standard suggests aligning revenue recognition with receipt of payments,except where collectability is uncertain.

B is incorrect.Current US GAAP includes extensive guidance on specific industries and transactions.The new standard moves away from this approach.

相關(guān)閱讀

延伸閱讀

以上就是【CFA財(cái)務(wù)報(bào)表分析練習(xí)題之利潤(rùn)表】的全部?jī)?nèi)容,如果你想學(xué)習(xí)更多CFA相關(guān)知識(shí),歡迎大家前往高頓教育官網(wǎng)CFA頻道!在這里,你可以學(xué)習(xí)更多精品課程,練習(xí)更多重點(diǎn)試題,了解更多最新考試動(dòng)態(tài)。